There can’t be much doubt any longer that over the past 15 to 20 years there have been some major shifts in the dynamics of commerce.

Or can there?

Surely, it must be a settled view that the on-line revolution which started a mere 15–20 years ago has changed the game.

Or is it? (and don’t call me Shirley)

Jokes aside (which is not easy for me…) I was surprised to learn during a recent chat with an associate of mine that perhaps for some things might not be as settled I thought. Cue dramatic sound effect and read on as our hero embarks upon another spirited tale of adventure and mayhem!

Let’s set the scene — My friend and I are in the partnership game. Or at least “partnership” in the sense of building new insurance distribution models based upon affinity. Affinity is an often misapplied term; but in my view the aim, in essence, is to look for commonalities or overlaps which might provide mutual benefit to the parties and their customers. As a focal point, I like to use what the marketing gurus at places like Google have termed “moment marketing”; or identifying points in a customer’s life where their propensity to buy or be interested in what you are selling is at its highest.

In this case, my friend saw an affinity between real estate and life insurance. The “moment” being either that time in a person’s life where they are considering the purchase of a home; or that time at which they have purchased a home and are interested in protecting their investment. Interested in pursuing a partnership distribution model in this space, my friend arranged for an introduction with the founder of a mature start-up real estate search platform in his home market. He then set about garnering the necessary internal stakeholder interest and approval.

The decision made by his company was not to move ahead with the partnership. I understand that several reasons were given, one or two were borderline reasonable — but one stood out to me as odd in this day and age. I paraphrase it below (the name and location have been redacted to protect the innocent and add just a soupcon of mystery to proceedings…)

“I had not heard of ######## prior to your e-mail.

From our initial checking — it seems that ####### is relatively unknown in ####### among locals…”

Now, granted, knowing who or what to partner with is not always an easy task; and you can’t partner with everyone. So at first blush maybe not having heard of them could be a reasonable metric. Then I thought about it some more — and although there may have been a time when that metric was relevant, that ship has sailed and it really is no longer valid.

I’m sorry, but it’s just not. And I’m not sorry…

The game has changed over the past decade to such an extent that not having heard of something is now not much more than a nasty case of confirmation bias. Using it as a threshold factor, demonstrates a failure to fully appreciate the shift in dynamics that has occurred over the past decade or so. If you’re fence sitting, allow me to unpack the notion and see if I can’t convince you {as an aside, I don’t want to be seen to impugn the decision highlighted above as a whole, the point rather is to isolate this particular reason and explore the shortcomings behind adopting it}…

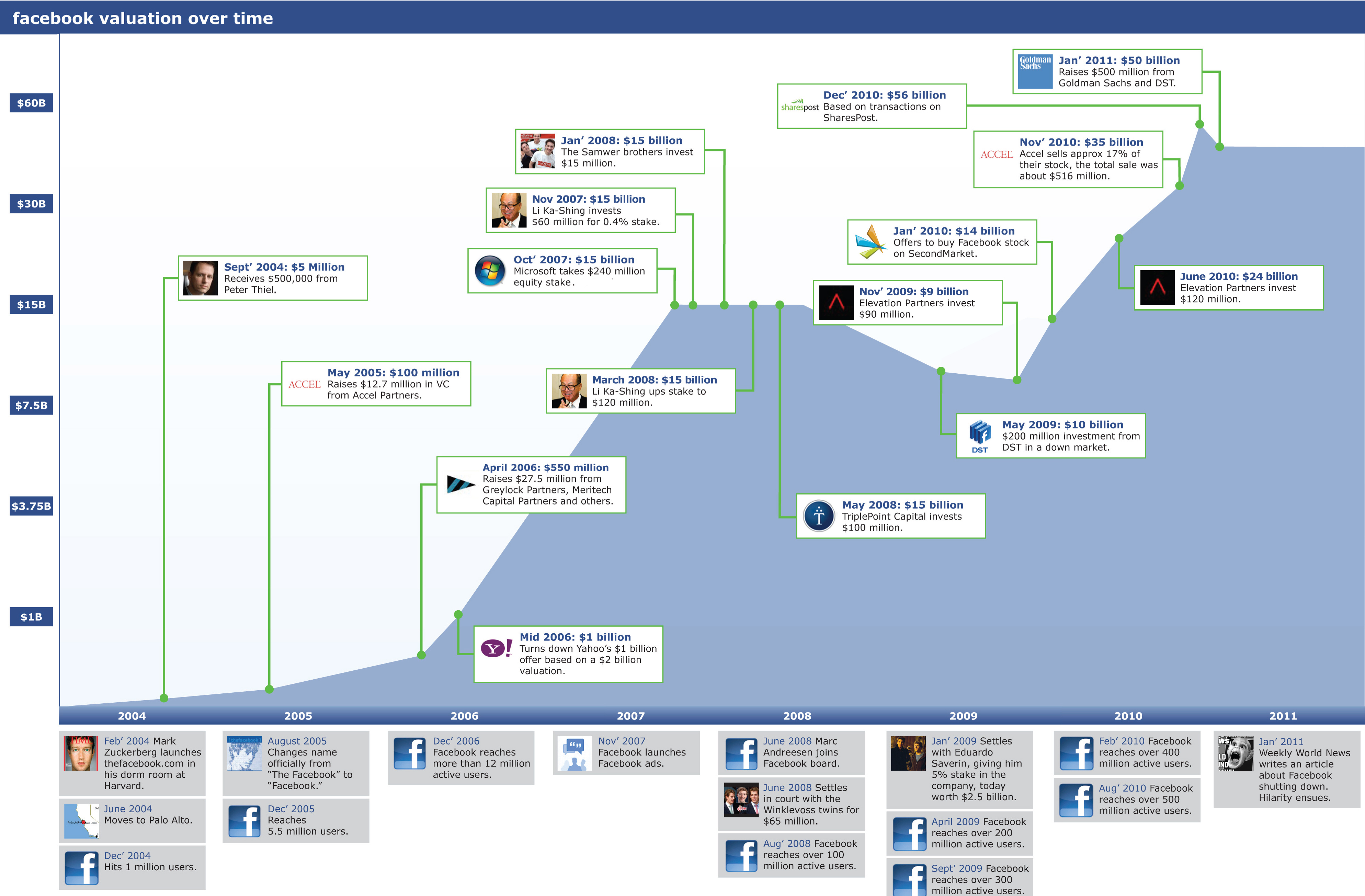

Let’s start by taking a brief trip down memory lane; to a time earlier this century when some brave new players wandered on to the stage. We’ll start not so long ago — mid 2005. A little known start up had attracted a few million users and changed its name from “The Facebook” to “Facebook”. If you turned them away at that point because of obscurity — you’d have watched it go from a USD100million valuation to USD24 billion. In less than five years. Bummer for you.

{kind=link}

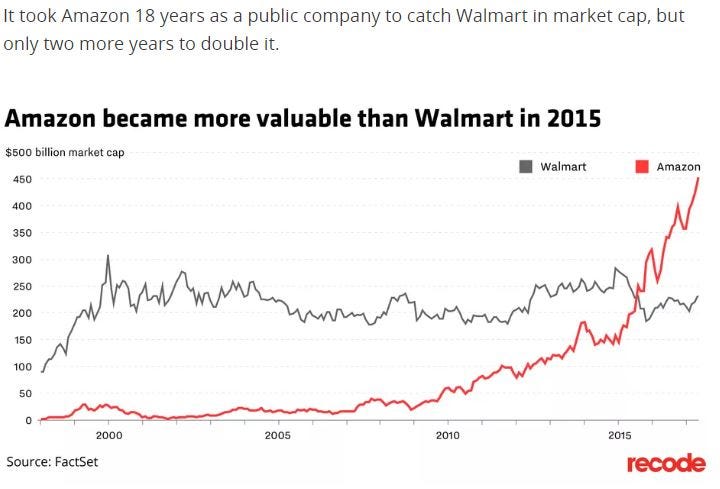

Of course, not nearly as big a bummer as missing Amazon. Which went from just a few billion in market cap in 2008 to USD250 billion in 2015. Extraordinary stuff! As this Recode article handily observes:

Lastly, let’s look at a company that’s been in the news recently — Lyft. Lyft completed its Initial Public Offering in the USA recently. Although the share price has not fared all that well after an initial flurry, those who got in early are set to be rewarded very handsomely indeed. A recent article on The Information revealed that a seed investor in Lyft from 2007 will see a nearly 10,000% return on its initial USD1 million investment.

Now you may be thinking that I am conflating equity investment with partnership. If you are then, sorry, but I’m not. I don’t think it’s too long a bow to draw to suggest that just like the early equity investors, those who were savvy enough to partner with these companies early will have reaped partnership gains of a similar exponential nature.

You might also think that the deployment of hindsight proves little or that examples like Facebook and Amazon lie very close to straw man territory in an argument like this. Maybe so, but I think the point remains well made: They were both entities which sprang from nothing doing something entirely new and if memory serves, were widely dismissed as mere flashes in their respective pans; and if you had used not having heard of them as the metric to turn them away, you’d be regretting it right now (to say the very least).

It’s not just that these dynamics that are shifting; so too are business models and methods. Technology is pushing customer experience, behaviour and preferences in ways not seen before. Tech is also driving down economic barriers to entry at an alarming pace meaning that the lines drawn to delineate traditional industries are becoming increasingly blurred. The move to platforms and ecosystems is inevitable. If you are not riding that wave now by exploring partnerships and lining up with other enterprises to form a platform, you are, to continue butchering my surfing metaphor, very probably doomed to sit out the back with the rest of the frubes.

Adding it all up, this combination means that not having heard of it is no longer a relevant decision metric. If you’re using it — abandon it. It will cause you to make mistakes. Start ups are now (and have been for a little while) the engine rooms of innovation and growth. Partnering with them is in all likelihood, key to your survival. As this article published in The Atlantic notes startups are now the driving force behind permanent changes to a “…nation’s whole economic structure.”

I think this quote from a post on MIT’s Sloan School of Management “Ideas Made to Matter” blog sums it up nicely:

“‘The world is changed by small groups of people who are committed, so I don’t think you should expect that innovation’s going to shift to not coming out of startups anytime soon,’ said Reshma Shetty, PhD ’08, the co-founder of Ginkgo Bioworks. ‘It’s an efficient innovation vehicle, so why run from that?’”

All of this reminds me of a cautionary and somewhat ironic tale told to me by an ex-colleague way back when I was working in the US in the midst of the first tech bubble in the late ‘90’s. He was working in Seattle for a large insurance brokerage. It was the late seventies and a small concern just starting up with a crazy idea to put a computer on every desk came to him looking for the standard suite of insurance products needed by any small business. He rejected them on the basis that they were too small.

To paraphrase something my hero, Winston Churchill is rumoured to have said — Is it not time to learn from history rather than being doomed to repeat it?

Lest I be seen as merely a dude in a glass house flinging pebbles telling war stories about the bloke who turned away Microsoft (did you guess right?), let me give some tips that might make decisions about partnership potential easier:

- Recognise that for better or worse the game has changed and you need to as well. Fundamental assumptions that might have held 10 or even 5 years ago are no longer valid. Think different!

- Adopt a venture capitalist mindset and take a portfolio approach. Don’t put all your money on one horse. Spread your bets across a number of runners. The theory being that out of ten investments the one that lands will more than make up for the nine that didn’t. Don’t believe me, have another look at the Lyft IPO Winners graph I linked above…

- There is an element of speculation required (see Tip 2!). There is risk. It may not work. There might be a leap of faith. That needs to be OK with you and along with it is the preparedness for failure. Failure is OK. But fail fast. Get on with it and move on.

- Speaking of fast, you’ll probably need to make decisions at speed and often without complete information. I get around that by having a set of minimum criteria designed to give decisions focus, logic, credibility and most importantly, speed. They are only 4 or 5 in number, but if a deal passes this “sniff test”, I very rarely go against it. The criteria are super robust. I know that even if it does go south down the track, application of them will give me a very sound chance of surviving future scrutiny (ie. my bott is covered). The only problem for you is -they are top secret! I developed them over many years of pain, failure, success, blood, wins, sweat, fun and tears. They are to me what the 11 secret herbs and spices are to the Colonel. But you can develop yours easily and that may even better suit your context. Start with a liberal dose of common sense and go from there.

- Lastly, if all else fails, go with your gut. Luckily I have a big one, so it’s easier for me. But if you don’t or even if you do, still listen to your gut. If it feels right, do it!

I appreciate that much of this may seen obvious, but I’ve noticed that often nowadays in the mad rush to find the woods, all many of us end up seeing are trees. So maybe its not so bad to be reminded of the obvious from time to time…

Good hunting!